The State of Toy Investing

Theorizing, Analyzing, Predicting, etc.

Hello friends,

I wanted to ramble a bit today about the current state of toy investing. A lot of things have been going on in the ecommerce space — not just in the last few days, but this entire year.

As we approach the new year, it’s important to look at the marketplace and try to get a feel for how it’s evolving and how we can position ourselves strongly going into 2025.

I want to start off by giving a strong opinion many may or may not agree with:

Right now, ‘Toys & Games’ is arguably the best category you can be prioritizing as a reseller.

I know it’s currently a sensitive subject with all of the recent restrictions in other categories like Beauty and Apparel, and I promise I’m not trying to kick others while they’re down. But really (my bias for toys aside) we are currently in such a strong position compared to other resellers in the ecommerce space. Let’s take a few things into consideration here:

Unless we are in a full blown apocalypse, there will always be demand for collectibles and discontinued toys. While many customers browse Amazon and select which toys they think look cool for a gift, a large part of our customer base is people looking for specific toys. A particular Spider-Man figure or a certain Monster High doll. Even if Amazon COMPLETELY told third party sellers to buzz off and restricted the ENTIRE toy category, our customers would follow us to the next best platform where they could find the collectibles they wanted.

Which leads me to my next point — there are more options for selling our toys than ever before. Walmart is the real deal. They are a direct threat to Amazon and will continue to steal market share from them. It’s no coincidence that Amazon announced they won’t be raising FBA fees in 2025 — they’re feeling the pressure. eBay is always thriving. It has never been easier to open a Shopify store. You can even host a toy sale at your home like a garage sale and people will travel to get some of the stuff we invest in (if the price is right). Heck, some people even open physical storefronts based on a single brand (LEGO). The point I’m making is that even in a worst case scenario, we have a lot more exit strategies than people who primarily focus on other categories. Any sort of brand restriction or account health issue will sting, but they won’t be as devastating as categories that have additional nuances like expiration dates or customers easily being able to browse to the next best thing (like they can with toilet paper or oatmeal).

Our average return rate is low. I don’t know about you guys, but I’m averaging a 3.1% return rate so far in 2024. The best part? Soooo many of these returns are able to be salvaged and re-sold on other platforms as ‘damaged’ or ‘loose’. That 3.1% return rate isn’t a true ‘unsellable’ return rate. Meanwhile, you have people in other categories with return rates as high as 15%! If you’re selling consumables or other products that can be ‘used’, you rarely are able to recoup that as easily as you can with toys.

Third party sellers are valuable to the toy marketplace and the big manufacturers know it. Imagine if every single toy completely vanished after manufacturers stopped producing them. Imagine there was no third party market for collectibles. Do you guys understand how much damage that would cause to the toy market? People collect because it’s fun — if you remove the fun aspect and don’t allow people to obtain older product, you completely kill hype for your brand. If you go through the list of the most valuable media franchises in the world, the vast majority of them have humongous collectible markets. The collectible market is valued at hundreds of billions of dollars. Again, the major manufacturers know this and understand that we provide a legitimate service to their fans. There’s a reason you don’t see Hasbro, Mattel, LEGO, Funko, and so many other brands filing claims against sellers on their discontinued product like you do in other categories — they want us to be there and fill that role.

Our main distributors are heavily connected to the manufacturers. We are one or two degrees of separation away from the teams who manufacture the products we sell. We are able to have influence on these manufacturers via our distributors because our supply chain isn’t (shouldn’t) be muddy. Our main distributors literally go to several of the manufacturer headquarters and present feedback on our behalf. I literally have been able to have manufacturers adjust production by using my distributor as a middleman. You just simply don’t get that with many other brands and categories, especially because the supply chains can be so much more complicated.

We have a ‘moat’ with toys — product knowledge. It is not easy for someone to just hop into toys and start making money. Having passion, excitement, and being a fan yourself of the products we sell is a competitive advantage that cannot be taught. It’s one thing to be able to look at Keepa and have it tell you if something is profitable or not. It’s another to understand why something is profitable, why something is popular, and if something is a good investment. People can’t easily just jump into our niche.

Now don’t get me wrong, ‘Toys & Games’ doesn’t come without its drawbacks. We aren’t selling hundreds upon hundreds of units a day of any SKU like some big players are in categories like Health & Household or Grocery. Our average profit per sale is nothing like some get on a $300 shoe. And we definitely aren’t in a niche that will make us rich quick. But like I said earlier, we carry so much less risk if something goes wrong that I’m willing to make less money for the sake of security. To me, having low risk and high upside is the best position to be in when running a business. Sellers that specialize in other categories may not necessarily be able to say they have the same safety nets as us.

I guess the point of the first part of this post is that even with all of the doom and gloom about Amazon lately, I just want to say that I’m excited to be 100% committed to this category going into 2025 and think we have very profitable times ahead of us — even in the unlikely event things go sideways.

The pendulum swing…

Next, I want to talk about a metaphorical pendulum swing that has been occurring in the toy market.

Let’s go back to 2020, right as COVID started to bring the supply chain to a halt. You may remember that everything was going out of stock and staying out of stock. There were so many delays that product just simply ceased to exist for months at a time. Due to the uncertain times, toy manufacturers were allegedly maximizing the amount of overseas production they could do because they weren’t sure when the next shutdown would be or when the next ship would be available that they could fill with containers.

This started a massive over-correction in production. Toys that should have only had 10,000 units produced were receiving production runs in the tens of thousands. That, in combination with movie theaters being intermittently shut down and many movie franchises releasing absolute duds, led to what seemed to be endless amounts of ‘collectibles’ being sent straight to clearance.

Shang-Chi into Eternals into Spider-Man: No Way Home (merch didn’t come out until the year AFTER release for Spidey) into Dr. Strange into Thor: Love and Thunder into Black Panther.

Years later, and you can literally still find Marvel Legends for $10 or less for almost every character from every single one of those movies (except Spider-Man). That streak of movies arguably could be the worst in terms of toy merch that Disney has ever had.

Retailers did not like this.

You also had this gem:

Yes, Funko literally over-produced to the point where they started physically destroying inventory.

But, it wasn’t just Marvel and Funko — it didn’t matter if you were McFarlane, Star Wars, WWE, or Jurassic — it was a dark time for merch sales (unless you were LEGO because their logistics are otherworldly and they had the Mexico manufacturing facility).

Fast forward to late 2023 / early 2024 and the supply chain is mostly healed, but manufacturers were taking a different approach now.

Instead of producing their product into oblivion, they decided to swing the pendulum again and over-correct in the other direction.

Rather than be stuck sitting on tons of inventory and having a bunch of retailers angry at them for giving them thousands of the same lame product, manufacturers started under-producing and discontinuing products sooner.

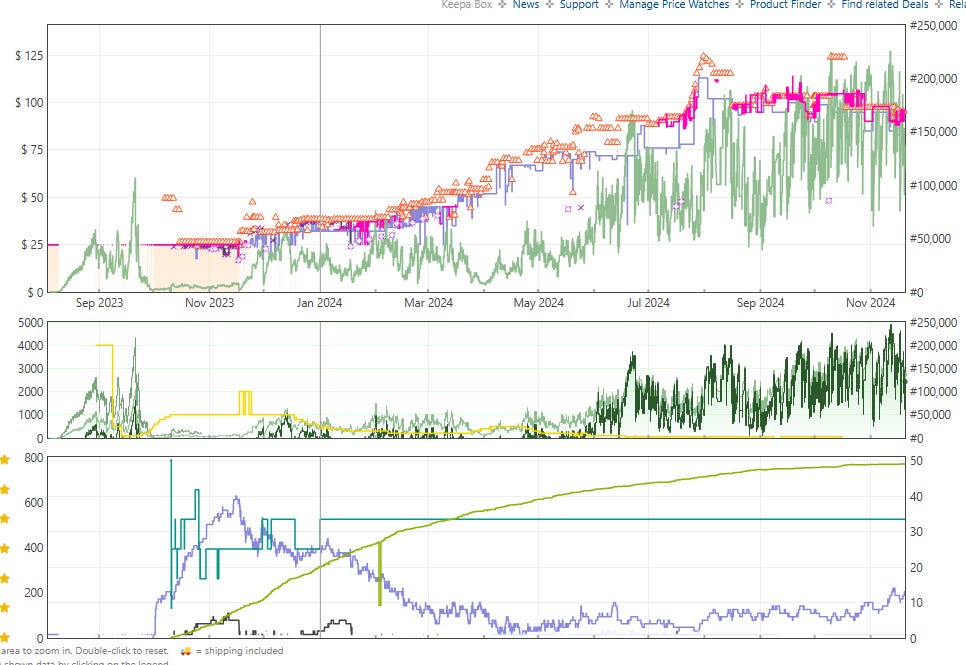

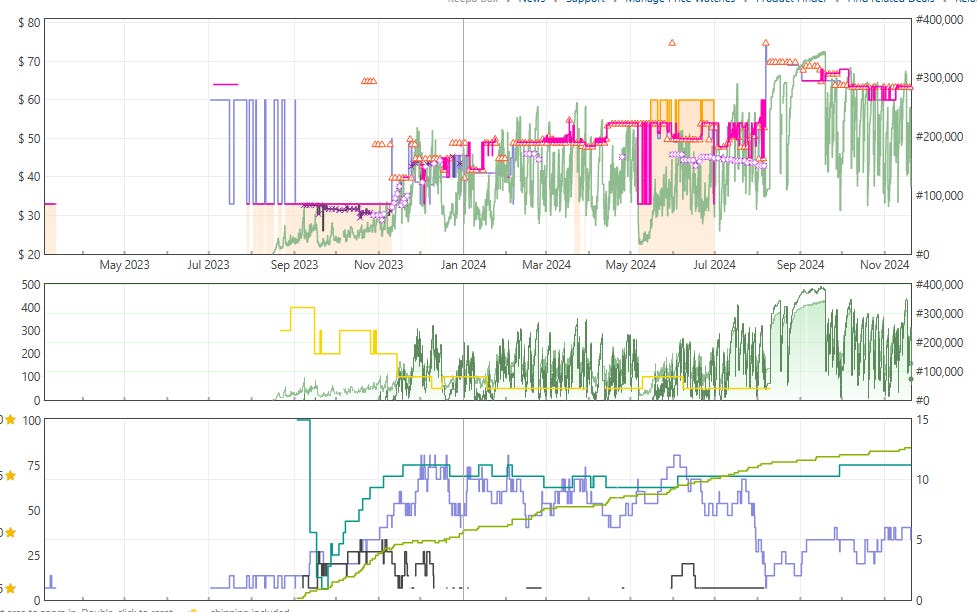

Notice something interesting about these toys?

(Just want to toot my own horn real quick, yes I invested in all of these)

All of them released around the end of 2023, saw their expected initial bump in sellers, and then never climbed up in sellers again — even though they were insanely popular! If you look at the previous years of data for toys from the same line, to not have a second or third spike in sellers (AKA another production run) was rare. But at the end of 2023 and early 2024 — it was common!

Manufacturers were truly under-producing figures of some very in demand characters. It was a goldrush opportunity!

So why does this matter and how does it affect us?

Well, unfortunately the mini-goldrush seems to be over. The pendulum was all the way to the right during COVID, swung all the way to the left at the end of 2023, and since around spring or summer it has slowly been making its way back to the middle.

What matters to us is that we are able to identify where we are in this pendulum swing — because it’s always swinging.

It seems now that manufacturers understood they were under-producing, so they’ve changed their production habits again.

Here is what I’m noticing (please keep in mind these are general, anecdotal points I am talking about and they don’t apply to every single toy line):